approaching")

Over the next few years, many buildings are set to become huge cost burdens as “stranded assets”. Why? Well, because of the future price regime for CO2 emissions. A relatively simple calculation reveals the potentially significant financial fallout investors and corporates face if they fail to take their environmental responsibilities seriously.

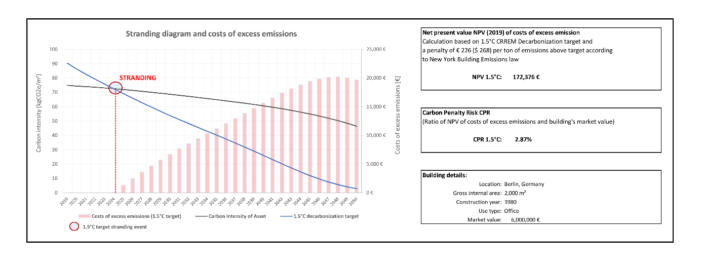

Take an example from Germany, according to numerous market surveys one of the most attractive markets for real estate investors in Europe and worldwide, and here specifically an office property in Berlin, built in 1980 with a gross floor area of 2,000 square metres. This building could incur additional costs of over EUR 172,000 by 2050 unless adequate decarbonisation measures are implemented to reduce or avoid emissions’ penalties. This “climate change penalty” corresponds to just under 2.9 per cent of the market value (EUR 6 million) of the property used in this example. The penalty imposed on the building is based on the scope of the fines contained in the recently enacted New York Climate Mobilization Act. Even if you only apply the penalty for fossil fuel emissions set out in the Fuel Emissions Trading Act, the building still faces additional costs of around 1.1 per cent of its market value. Anyone who has a rough idea of the current returns that can be generated by our sample property will probably break out in a cold sweat when they read this. And it could get even tougher, since the latest findings of the Intergovernmental Panel on Climate Change (IPCC) require much more focused action than has been seen in the industry so far.

CRREM provides clarity

Our sample calculation above is based on findings and benchmarks from the Carbon Risk Real Estate Monitor project (CRREM for short), which is supported by the European Union (EU) and a consortium of industry-leading real estate investors. Taking empirical data on the maximum available global emissions budget that is compatible with the Paris climate goals, the CRREM project for the first time developed national and segmental decarbonisation pathways to enable the real estate industry to identify and quantify environmental risks (“carbon risks”) and take appropriate action to mitigate them. As a reminder: According to the World Green Building Council, if we want to to comply with the Paris Climate Agreement and limit global warming to well below 2.0°C (ideally 1.5°C) compared to pre-industrial levels, every building will need to be CO2-neutral by 2050. The EU and its member states are pushing this goal by introducing a raft of new regulations. Plans to price emissions are one measure that will be introduced to help achieve this goal – in the knowledge that it will hit companies where it hurts.

The “stranding moment” is no more than a few years away

Reducing CO2 emissions from existing buildings requires investment – and it needs to happen quickly. Depending on which scenario you apply, the Berlin office building cited above is at risk of becoming a stranded asset as early as 2024 – unless suitable countermeasures are implemented. Without action, the buildings’ greenhouse gas emissions will exceed the levels permitted by a decarbonisation target of 1.5°C by 2050. If we assume a decarbonisation target of 2.0°C, the stranding moment will not occur until 2030. But even in this case, the costs of the building’s excess emissions would still be enormous: the net present value of the costs of the property’s surplus emissions would total almost EUR 99,000, equivalent to almost 1.7 per cent of its market value.

Figure: Many buildings are at risk of becoming stranded assets over the next few years

In-house calculation, based on CRREM

Increase transparency or pay the price

Asset managers and corporates simply cannot afford costs on this scale. There is a window of opportunity to minimise the financial fallout – but it is closing fast and action is required. Crucially, real estate owners and operators need transparency. They first need to determine the extent of the emissions from their individual properties and entire portfolios if they are to have any basis for meaningful action at all.

This is where data play a key role. In order to generate actionable insights, you need structured and systematised data. And these date must not be limited to individual buildings. Investors, asset managers and corporates generally own or manage a number of properties, so they need a portfolio-level perspective. They also have to deal with large volumes of data from disparate data sources, systems and standards. Current methods and tools either tend to represent isolated, stand-alone solutions or are fast approaching the limits of their capabilities. As far as BuildingMinds is concerned, the real estate industry needs a single platform and Common Data Model to tap the potential of data, because it is only through data standardisation and harmonisation that we can master the increasing complexity of real estate and portfolio management. In particular, this also applies to the development and implementation of decarbonisation strategies. Moreover, the sustainable management of real estate doesn’t just reduce risks and mitigate the threat of upcoming emissions levies or the even more punitive penalties for greenhouse gas emissions coming our way in the very near future. It also represents a pathway to asset optimisation and, when done right, can even increase the profitability of your real estate investments.