At Cannes for MIPIM 2026, Europe’s largest real estate conference once again compressed a year’s worth of market sentiment into a few intense days. This year, one thing struck our team: it felt like there were two conferences in parallel.

Talking with people, the mood was still sombre. Middle Eastern representation was notably down, shadowed by the ongoing conflict in Iran. But elsewhere, the energy was different, more buoyant than in recent years. Perhaps still not “business as usual,” but packed calendars, crowded terraces, and a renewed urgency to deploy. At times, it seemed as though attendees were at entirely different events.

That contrast captures something important about where the real estate industry now finds itself. A clear picture emerged from our conversations over the week: we’re no longer operating within a single cycle or a single narrative. Instead, the industry is navigating the intersection of slower capital markets, geopolitical fragmentation, and rapid technological change. And while each of those forces matters on its own, it’s their interaction that is reshaping the outlook for the industry.

A market in transition

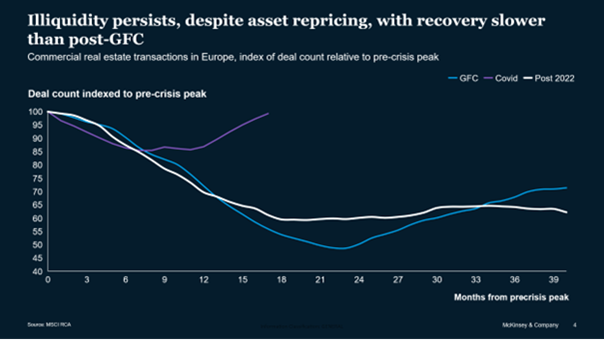

Liquidity remains below historic norms. The downturn has been shallower than the post-global financial crisis correction, but the recovery has also been slower. This means that while the industry hasn’t found itself in widespread distress, it hasn’t been particularly liquid either for several years.

In the past, we often framed disruption in terms of what was cyclical versus what was structural. That distinction still has value, but it no longer feels sufficient. Today, real estate leaders are also contending with broader global forces, especially geopolitical fragmentation and the rise of AI, that cut across both categories. These feel less like cyclical waves and more like an overwhelming tidal movement.

Geopolitics moves centre stage

Geopolitics has shifted from background noise to a core strategic concern. There was broad recognition at MIPIM that fragmentation is beginning to reshape capital flows, with the forward outlook suggesting that the preference gap between Europe and North America has largely closed. Conflicts are more prevalent, and the sense of operating in an era of relatively stable global order has faded.

Trade and industrial policy are becoming more national, especially in defence and strategic sectors. Cross-border flows of capital and labour are facing new constraints and consensus around global priorities, particularly climate change, is becoming harder to sustain.

For investors, this changing backdrop is altering behaviour. LPs are recalibrating risk appetites and profiles. The direction of travel isn’t towards safety at all costs, but towards more modest and more legible risk profiles. Core+ and value-add strategies are attracting renewed interest. Meanwhile, according to McKinsey’s annual survey of ~300 LPs, appetite for opportunistic risk-return profiles as well as lowest risk super-core has reduced noticeably in the last year. The implication isn’t a retreat from real estate, but a more selective search for returns in a world that feels less predictable.

From asset allocation to product excellence

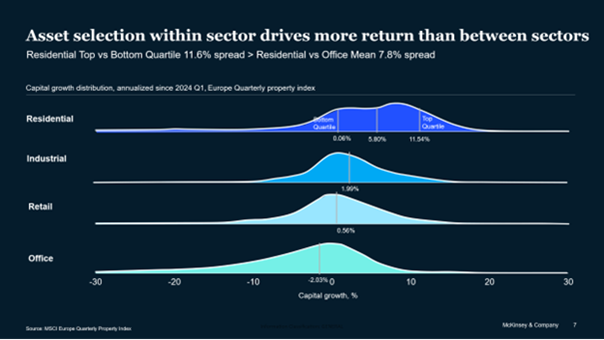

That selectivity is also showing up in how performance is discussed. One recurring theme at MIPIM was that returns are increasingly driven less by allocation between sectors and more by performance within them. In other words, the source of outperformance is shifting from choosing the right category to creating the right product.

This points to the continued rise of “real estate as a product” rather than simply “real estate as a financial asset.” The quality of the operating model, the relevance of the offer, and the ability of an asset to meet specific user needs are becoming more important differentiators than broad sector exposure alone.

AI: From promise to practice

Alongside geopolitics, AI was the topic that repeated again and again—both in terms of what it can do for the industry today and what it may mean for society more broadly.

At the practical level, many discussions centered on one question: how do we practically and successfully capture value from AI today? The answer always comes back to fundamentals. Better AI outcomes require better data architecture and management: more robust, more structured, and more accessible data. They also require clarity on which processes truly matter, so leaders can decide which should be standardized, which can be automated, and where technology can genuinely improve decision making.

In an industry that often operates with relatively lean teams, the challenge is selecting the right areas of focus, with clear ROI and leadership support to justify investment.

A provocative debate I had a few times over the weekwas whether AI has reached the point where a newly established company could build a far more automated, efficient, and effective management platform from scratch, and do so at a meaningfully lower cost than an incumbent burdened by legacy systems and ways of working. What would that take to achieve and what would it mean for the competitive dynamics of the market?

The question for established players is not just whether that happens, but how quickly they can respond if it does.

Broader implications

Beyond operational domain applications for AI, conversations often expanded into broader questions about business models, investment assumptions, and social impact. What happens to SaaS economics when agentic workflows can be rapidly and cheaply created? What does that mean for private equity investments underwritten on the basis of five- to ten-year cash flow growth if competitive moats become less durable and disruption cycles shorten? And beyond capital markets, what will this mean for our children, their careers, and the social contract around work?

Building anti-fragile portfolios

Set against that uncertainty, a final thread ran through many MIPIM conversations: how can real estate position itself not just to withstand disruption, but to benefit from it? How do we build portfolios and companies that are not just resilient to the disruption we face, but are anti-fragile, structured in ways that allow them to strengthen as volatility rises?

That requires multiple moves at once. It means seeking outperformance through superior asset performance within sectors, not relying only on sector rotation. It means identifying and selectively overweighting areas aligned to major global trends, data centres linked to AI, logistics tied to supply-chain resilience, or infrastructure connected to defence and national industrial priorities. And it means using AI not as an abstract theme, but as a practical lever to improve the speed and accuracy of decisions while protecting trust and judgement.

Looking ahead

These conversations suggest an industry entering a new phase. Real estate is still cyclical, and structural questions still matter. But leaders must now navigate a wider set of forces that are less correlated, less stable, and more consequential than before. In that world, the winners won’t be those who wait for clarity. More likely, they’ll be the ones who redesign and build the capabilities, portfolios, and operating models that allow them to move quickly and with conviction even when the environment remains unsettled.

After a week of intense conversation in Cannes, that’s the challenge we are taking back with us. And it’s one we expect will define the industry for years to come.